November 25, 2022

Supporting alignment with the Paris Agreement through investing in carbon removals

Sustainable nature-based solutions provide a ready, proven and economically feasible solution for carbon removal, writes Marko Berglund, our Senior Impact Adviser.

The growing need for carbon removals

The IPCC says it loud and clear: limiting warming to 1.5°C or 2°C will require rapid, deep and immediate cuts in emissions in all sectors of the economy. Even this will not be enough, however, as residual emissions will need to be removed from the atmosphere. While carbon capture and storage (CCS) has been suggested as a solution for carbon removal, and may be more ready to be taken up in some sectors than others, CCS faces several barriers, including technological, economic, institutional, ecological-environmental and socio-cultural issues. In addition, rates of CCS deployment are far from the scale of what would be required to meet the targeted pathways. Sustainable nature-based solutions, on the other hand, provide a ready, proven and economically feasible solution for carbon removal; afforestation, reforestation, improved forest management, agroforestry and soil carbon sequestration are currently the only cost-effective widely practiced removal options available.

A strategy aligned to deliver

Finnfund recently updated its strategy for the period 2022 – 2025. The strategy is framed against global impact themes, one of which is climate action. This theme is also reflected in Finnfund’s three key strategic objectives, one of which is to maintain a carbon net negative portfolio. In turn, investments in forestry, which is one of Finnfund’s priority sectors, form the backbone and provide a strong illustration of effective and credible carbon removals financing.

Standards are evolving

There is, as yet, no overarching method for calculating portfolio removals agreed under the GHG Protocol / PCAF guidance. To fill this gap, Finnfund engaged in 2021 with Swedfund, BII and FMO to develop and launch FRESCOs, an open-source tool to calculate emissions removals. The methodology is available on the FRESCOS website. The tool uses company specific forest inventory data; the quality of this data is comparable to the emissions data Finnfund reports. The main challenge is company buy-in and access to their operational data, at the required level of accuracy. Without accurate calculations also on the removals side, consolidated portfolio data will be challenging to compile. Going forward, one main challenge will be to apply continuously evolving and developing standards; changes also make it difficult to establish reliable and comparable time-series of emissions / removals data.

Adding it all up

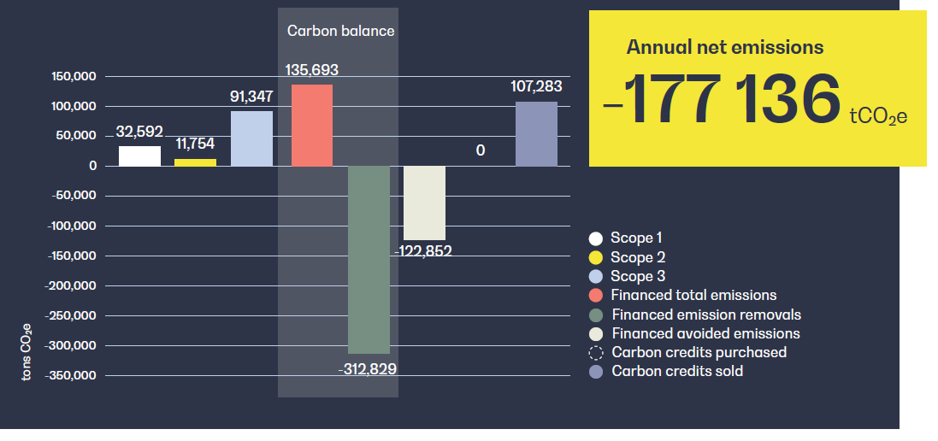

As outlined above, Finnfund measures and reports its portfolio carbon emissions and removals using transparent methodologies. Applying these methodologies, Finnfund has calculated that its investees’ Scope 1, 2 and 3 (upstream) emissions were 135,693 tCO2e in 2020, which is the latest year figures are currently available. A large majority of these emissions were investees’ Scope 3 upstream emissions. Alongside these financed emissions, Finnfund’s financed emissions removals, estimated using FRESCOs, were 312,829 tCO2e. This means that in 2020, Finnfund’s financed emissions removals were 177,136 tCO2e more than its financed emissions. In other words, at an aggregate level, when attributed to Finnfund, Finnfund’s investees, including their upstream value chains, removed more carbon from the atmosphere than they emitted. In addition, for full disclosure and transparency, Finnfund also reported in 2020 that it financed 122,852 tCO2e of avoided emissions, and that its investees sold 107,83 tCO2e of carbon credits.

Climate impact of Finnfund’s portfolio in 2020.

What next for portfolio emissions?

Going forward, as part of its current strategy, Finnfund will continue to finance more carbon removals than it finances emissions. This is in large part due to its forestry portfolio; Finnfund has been investing in forestry projects since its inception. As more DFIs and other investors move into the sustainable forestry sector for climate as well as other reasons, several issues need to be borne in mind. First, sustainability is key. Afforestation and reforestation activities should not conflict with social or environmental objectives. For Finnfund, in practice this means that all of our forestry investments are FSC certified. Second, forest growth cycles are key elements when looking at portfolio carbon removals. While afforestation and reforestation projects remove carbon during projects’ early years, revenue from harvesting is created only once forests reach maturity. Patient capital and carbon credits are key for sustainable forestry projects to ramp up to the level needed for IPCC targets. Third, as outlined above, carbon removal methodologies are still being developed and updated, which may affect carbon accounting also for financial institutions. During this debate, it will be important to distinguish the role of emissions and removals in the real economy, compared to the role they play in and for financial institutions. In whichever ways methodologies are framed, it is clear that just as we need all possible emissions reductions and removals, we also need funding from various and diverse sources to carry out climate projects, which may otherwise not go ahead. Financing emissions removals should conceptually be delinked from carbon finance, as financing emissions removals and financing carbon credits aren’t necessarily counted towards the same types of climate commitments. Placing both forms of finance on the same line potentially means either cutting off removals finance, or cutting off carbon finance, both of which are often needed for projects to be viable.

CASE STUDY – Data availability and quality is key

Finnfund joined the Partnership for Carbon Accounting Financials in April 2022. While Finnfund has yet to make its first disclosure under PCAF, it has already been applying PCAF methodologies. PCAF provides a solid and comparable set of measurement guidance, which attributes Finnfund’s share of financed emissions in line with common standards. PCAF builds on and cross-references other standards, such as the Greenhouse Gas Protocol, ensuring compatibility and conformity across actors. The GHG Protocol defines three scopes of emissions: Scope 1 emissions are direct emissions from sources owned or controlled by a company, Scope 2 emissions are emissions generated through the purchase of electricity / heat consumed by a company, Scope 3 emissions are all other indirect emissions. Scope 3 emissions are further divided into several categories: Scope 3 category 15 emissions are fundamental from a financial institution’s perspective, as they include the FI’s portfolio emissions (which are further split into Scope 1, Scope 2 and Scope 3 emissions). Finnfund strives for data quality and works with its investees to base its accounting as far as possible on primary data. As with many of its peers, the closer Finnfund is to its emissions sources, the more accurate its data is. For example, Finnfund’s investees’ Scope 1 and 2 emissions are measured either through reported emissions or, when this is not possible, calculated through physical activity-based emissions. For investees’ Scope 3 emissions, Finnfund often needs to estimate and model emissions based on economic activity.

Marko Berglund

Senior Development Impact Adviser

Marko Berglund is a Senior Development Impact Adviser at Finnfund. He has worked for several years with climate and carbon finance.

This text, originally published by EDFI, Association of European Development Finance Institutions, is part of a collection of essays that build on key themes related to impact and DFIs. These essays are intended to supplement, and to engage in dialogue with, the discussions at EDFI’s annual Impact Conference 2022, and to address the same overarching topics.

Sources:

IPCC, 2022: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA. doi: 10.1017/9781009157926

IPCC, 2022: Climate Change 2022: Impacts, Adaptation, and Vulnerability. Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [H.-O. Pörtner, D.C. Roberts, M. Tignor, E.S. Poloczanska, K. Mintenbeck, A. Alegría, M. Craig, S. Langsdorf, S. Löschke, V. Möller, A. Okem, B. Rama (eds.)]. Cambridge University Press. Cambridge University Press, Cambridge, UK and New York, NY, USA, 3056 pp., doi:10.1017/9781009325844.

FRESCOS, Free Web Tool for Carbon Sequestration Calculation, https://www.frescos.earth, accessed 24.10.2022

PCAF (2020). The Global GHG Accounting and Reporting Standard for the Financial Industry. First edition. November 18, 2020

Read more

Climate accounting – our work in practice

Climate accounting – our work in practice

Climate effects

Climate and Energy Statement (pdf)

Annual Report (incl. Climate action – Task Force on Climate-related Financial Disclosures)

Finnfund first development financier to report carbon net-negative investment portfolio

Sustainability Policy