Climate accounting – our work in practice

Climate change mitigation and adaptation are among Finnfund’s key objectives and development achievements. This work is based on our Sustainability Policy, Exclusion list, and Climate and Energy Statement.

Climate change mitigation and adaptation are among Finnfund’s key objectives and development achievements. This work is based on our Sustainability Policy, Exclusion list, and Climate and Energy Statement.

Finnfund assesses the climate effects of every investment as part of the investment process leading to an investment decision, as well as annually during each respective investment period. This includes an assessment of the absolute emissions of investments, avoided emissions of energy investments, and carbon removals of forestry projects.

This article summarizes and explains the process and methods for climate accounting of Finnfund investments – step by step.

“Finnfund’s carbon accounting stems from our desire to understand better the climate impacts of all our investments, as mitigation of and adaptation to climate change are among the key objectives of Finnfund

“Finnfund’s carbon accounting stems from our desire to understand better the climate impacts of all our investments, as mitigation of and adaptation to climate change are among the key objectives of Finnfund

– Kenneth Söderling, Development Impact Adviser

Climate accounting at Finnfund.

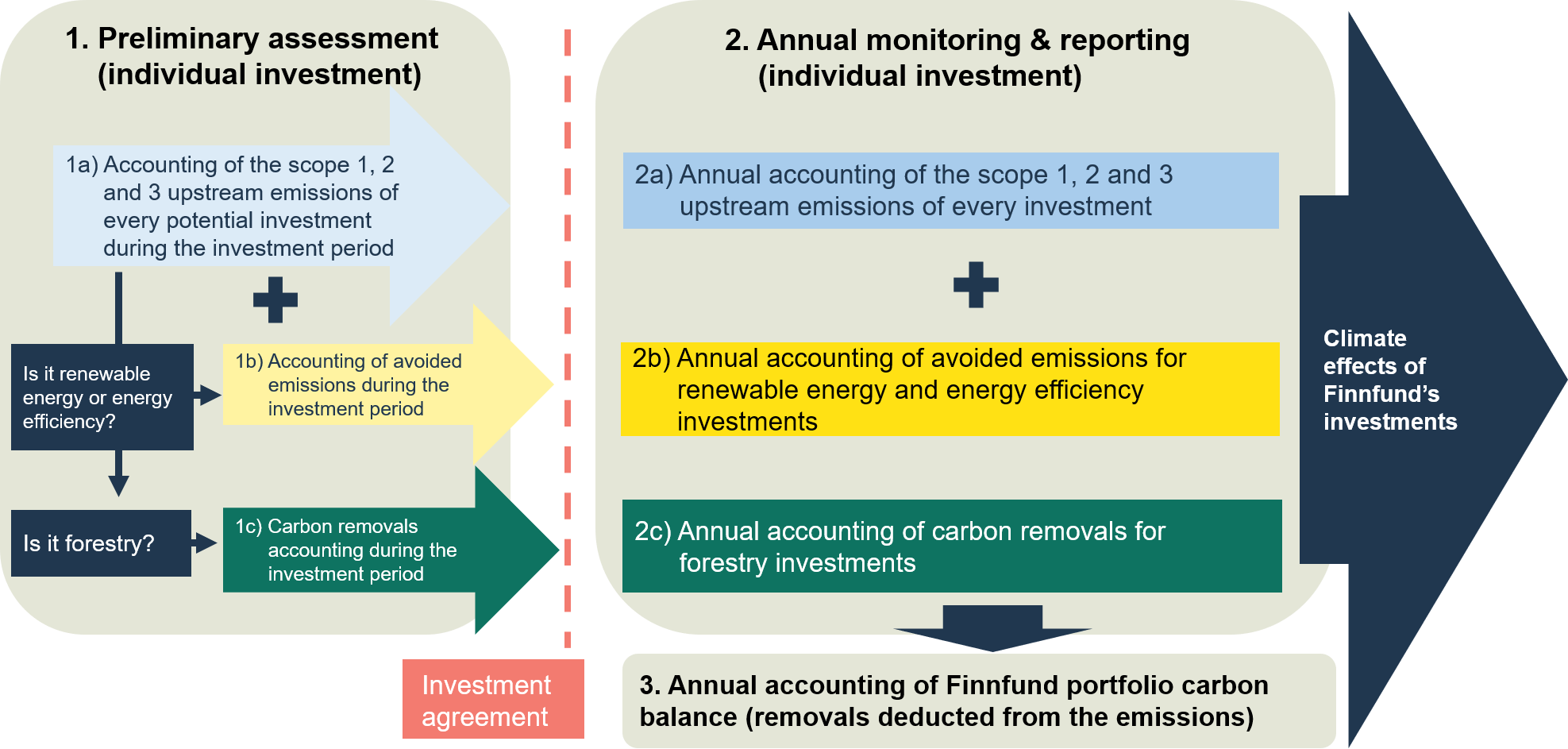

1. Preliminary review

As part of its investment process, Finnfund assesses the climate effects of every potential investment prior to an investment decision.

In addition to assessing the climate effects of every investment, Finnfund also assesses investments against the framework of the Paris Agreement.

1.a) Emission accounting for every investment

Prior to the investment decision, as part of the due diligence process, Finnfund assesses the scope 1, Scope 2 and upstream Scope 3 climate effects of every potential investment. In other words, Finnfund takes into account the direct and indirect emissions of each company’s production (Scope 1), energy consumption (Scope 2) and purchased services (upstream Scope 3). Downstream Scope 3 emissions are only considered if Finnfund invests in a high emission intensity sector, which has major scope 3 downstream emissions.

Finnfund’s climate accounting is based on the GHG Protocol, and Partnership for Carbon Accounting Financials (PCAF). Finnfund is a signatory member of PCAF, which it joined in April 2022.

Climate effects are attributed to Finnfund according to the PCAF standard. Based on these rules, climate effects are reported only for the time period when Finnfund is actually financing an investment. If, for instance, Finnfund’s financing share in a forestry company that removes carbon from the atmosphere decline (a loan is partly repaid, for example), Finnfund’s reported carbon removals would decline as well, even if the company would continue removing carbon as before.

Finnfund follows the principles of absolute accounting, which means that we do not deduct possible carbon offsets from our companies’ accounted emissions. While Finnfund does not recognise compensation or carbon offsets as part of its portfolio emissions or removals, in order to increase reporting transparency, Finnfund collects data on carbon credits sold by its forestry investments, and carbon credits bought by all investments, and discloses this information as part of its annual report.

Finnfund uses primary emissions data or energy intensity data, whenever it available, to assess investments’ emissions. When such data is not available and an investment is not considered to have a high climate effect, Finnfund uses the Joint Impact Model (JIM) to estimate emissions; its input / output model takes into account emission factors per million euros of revenue of certain sectors and countries/regions. In line with Finnfund’s conservative approach to climate accounting, the JIM model over- rather than underestimates an investment’s emissions.

Investments which are considered to have high climate effects, e.g., large investments (>7.5 M€), investments for high emissions sectors (see annex 1), or investments with land conversion (>100 hectares), are accounted with a GHG accounting tool which uses reported primary emission or energy data.

The sectors with high climate effects include e.g.

- Air transport

- Basic metals

- Building materials

- Chemicals

- Chemicals and chemical products

- Coal mining and peat harvesting

- Coke and refined petroleum products

- Electricity, gas and steam supply

- Electric power generation

- Extraction of crude petroleum and natural gas

- Fabricated metal products

- Fertilizer products

- Data centers

- Glass and glass products

- Meat and dairy production

- Mining of metal ores

- Other chemical products

- Other mining and quarrying

- Plastics products

- Pulp, paper and paperboard

- Rubber and plastic products

- Transport

- Waste collection, treatment and disposal

1.b) Accounting of avoided emissions for renewable energy and energy efficiency investments

For companies operating in the renewable energy sector and/or contributing to increased energy efficiency, Finnfund assesses avoided emissions as part of its investment decision process.

For avoided emissions, Finnfund follows the International Financial Institutions Technical Working Group (IFI TWG) on greenhouse gas accounting instructions.

The avoided emissions of grid connected projects are accounted by using the IFI TWG grid emission factors as a baseline. For energy efficiency projects, a project specific baseline is used according to IFI TWG instructions. Avoided emissions are attributed according to the PCAF.

1.c) Accounting of carbon removals for forestry investments

For companies operating in sustainable forestry, Finnfund assess emissions removals as part if its investment decision process. Removals are accounted using the publicly available FRESCOS tool, which Finnfund developed together with fellow development financiers and AFRY, a consultancy. The FRESCOS methodology is based on IPCC Guidelines for National Greenhouse Gas Inventories: Volume 4 Agriculture, Forestry and Other Land Use (2006).

Finnfund accounts the carbon stock changes of above and below ground biomass, dead organic matter, harvested wood products and soil. Soil carbon stock changes are based on IPCC default values.

2. Monitoring and reporting

Finnfund accounts, monitors, reports and attributes the climate effects of every investment during the entire investment cycle on an annual basis.

2.a) Monitoring the emissions of every investment

When monitoring companies’ emissions, Finnfund uses primary emissions data or energy intensity data, whenever it available. When such data is not available, Finnfund uses the Joint Impact Model (JIM) to estimate emissions.

As the model is based on revenue / emission factors, the emissions generated during the construction period are excluded.

Finnfund requires companies with high emission levels to conduct carbon accounting. If a company is not able to carry out the accounting by themselves, Finnfund will account the carbon footprint with the GHG emission accounting tool from the energy use data provided by the company.

2.b) Monitoring avoided emissions

Finnfund continues to account and monitor avoided missions of companies operating in the renewable energy sector and / or contributing to increased energy efficiency.

2.c) Monitoring carbon removals

Finnfund continues to account and monitor carbon removals of companies operating in the forestry sector.

Finnfund accounts the annual changes in various carbon stocks, such as above and below ground biomass, dead organic matter, harvested wood products, and soil organic matter.

Some forestry companies in Finnfund’s portfolio produce and sell harvested wood products. This wood product stock is accounted by Finnfund as a carbon removal; the question of whether this stock is also part of a third party’s GHG inventory is currently being discussed.

Finnfund closely follows the development of the GHG protocol land sector and removals guidance and is willing to develop further our approach in the future if necessary.

3. Carbon balance: climate effects of Finnfund’s investment portfolio

Finnfund also accounts its portfolio’s net climate effects annually and publishes these results in our Annual Review.

Finnfund’s carbon balance is calculated by deducting the annual carbon removals from annual carbon emissions of its portfolio.

Finnfund does not include avoided emissions or carbon credits as part of its carbon balance. The assessment of avoided emissions is based on a scenario analysis and does not represent an absolute effect; hence they are not taken into account in the carbon balance. Carbon credits are not absolute effects either, and therefore these are not taken account on either side of the balance. Both avoided emissions and carbon credits bought / sold are, however, reported to increase transparency, as per international best practice.

More information

Climate effects

Climate and Energy Statement (pdf)

Annual Report (incl. Climate action – Task Force on Climate-related Financial Disclosures)

Finnfund first development financier to report carbon net-negative investment portfolio

Sustainability Policy

Interested to know more about our work in practice?

Human rights management system – our work in practice

Responsible tax principles in practice – our work in practice

Kenneth Söderling, Development Impact Adviser, tel. +358 40 358 6139, kenneth.soderling@finnfund.fi

Marko Berglund, Senior Development Impact Adviser, tel. +358 50 433 6458, marko.berglund@finnfund.fi