December 22, 2021

Client protection in microfinancing is part of financial inclusion

Microcredit and microfinance refer to very small loans for individuals or micro-businesses. In some context, it refers to other services as well such as micro-insurance, micro-pensions, micro-leasing, and even micro-savings.

More importantly, it is about providing access to formal financing and participation for people in need of money to set up or expand their businesses. It is also a chance for financial inclusion, to be a participating member of the community. Therefore, in many countries microfinance institutions (MFIs) are monitored by regulators just as the normal banks.

Responsible lending practices are key

Microfinance is an instrument to help people to engage in income-earning activities and increase financial resilience against unexpected crises. It is expected to contribute to social and human development and to enhance empowerment, especially of women. However, if not well structured and managed, microfinance may also have negative impacts: the borrowers may, for instance, struggle with money and face the risk to become over-indebted by participating in more than one microloan scheme, or by falling in the hands of loans sharks, or risking their business or personal assets being confiscated in case of default.

Therefore, it has been understood that microcredit is only the first step to financial inclusion. Microfinance must always be based on responsible, sustainable lending practices and respect. In practice, it means, e.g. financial education, client-friendly procedures, financial services with fair pricing, easy access to opening accounts, and transferring money. It is clear, that in this context human rights need to be considered particularly in terms of the rights of minorities and other vulnerable groups. Education and knowledge sharing also on data privacy must be enforced.

To respond to these needs the SMART Campaign was a global initiative from 2009 to 2020 to protect the MFI borrowers and to provide the tools to MFI organisations to deliver transparent, respectful, and practical financial services to all its clients. Finnfund has included the SMART Certification requirement in all microfinance investments since 2013.

The potential gaps of client protection are identified in the environmental and social due diligence process. Our investees may not always meet all criteria at the beginning, but during the investment lifecycle, they are guided to work towards the certification.

New framework for client protection

As The SMART Campaign, containing its Client Protection Standard and management, came to its end in April 2021, an important question arose: what would be the next internationally recognised framework and certification for sustainable microfinance?

In April, The SMART Campaign was transferred to The Social Performance Task Force (SPTF) and Cerise, a French NGO pioneering in social performance management. These organisations were always part of the SMART Campaign audits and certification providers. There will be no more renewals of the SMART certification, but the same principles are now included in The Client Protection Pathway which was launched in October 2021.

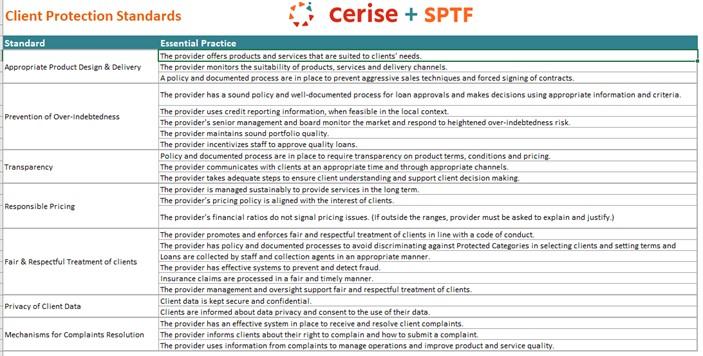

The new framework covers seven key standards/areas: appropriate product design and delivery, prevention of over-indebtedness, transparency, responsible pricing, fair and respectful treatment of clients, privacy of client data, and mechanisms for complaints resolution. In the picture below, you may see the content of each of them in more detail.

Client Protection Pathway in a nutshell.

Finnfund is committed to The Client Protection Principles

Finnfund currently provides funding for 10 microfinance institutions in Asia and Africa. We commit to the new Client Protection Pathway the same way we did with the SMART Campaign, requiring contractually our investees to work towards or to maintain the already achieved certification status.

Client Protection Principles provide straightforward standards and clear guidance to the MFIs on how to achieve this. In most cases, they are happy to formalise the commitment and work towards the public signatory status, as they see the value to their business and often already follow similar practices. Increased trust and financial literacy among borrowers strengthen the business relationship and may also have positive impacts on the brand.

As always when new initiatives appear, the environmental and social experts from many European development financiers (EDFIs) have been discussing informally the new Pathway and possible alternatives since February 2021. Finnfund has facilitated these regular, voluntary virtual meetings. These discussions have provided us valuable insights on the topic and a forum to discuss common guidelines and practices.

As the Client Protection Pathway is now launched and already familiar to many of the microfinance and financial institutions we finance, Finnfund will currently base our client protection approach on the SPTF/Cerise Client protection pathway. We acknowledge that both the pathway and the field of client protection will evolve, and we continue to closely follow these developments.

For instance, it is already clear that in the changing world where climate change impacts us all, the principles are being expanded and developed towards including environmental as well as labour requirements. Eventually, the micro-insurance, fintech, off-grid solar, and other sectors where client protection is important will also be included.

Riikka Thomson

Manager, Environmental and Social

Read more

Financial institutions – Finnfund

Case: Jumo – Finnfund

Case: BOPA – Finnfund

The Client Protection Pathway

Comments

Comments are closed.

It is very impressive for the Finish government to take up that challenging role around the globe . I am happy to say that your government . I am willing to be one of the Micro Finances which are part of your support .

Thank you for your feedback! You may find our investment criteria, contact details etc. here https://www.finnfund.fi/en/investing/sectors/financial_institutions/ and https://www.finnfund.fi/en/investing/looking-for-an-investor